M-Pesa launched in Kenya on March 6, 2007, as a basic mobile money transfer tool. Nearly two decades later, it has transformed into Africa’s largest fintech platform, playing a pivotal role in establishing Kenya as the continent’s renowned Silicon Savannah.

Based on recent data, the platform processes over $400 billion in transactions annually across a network of more than 660,000 agents.

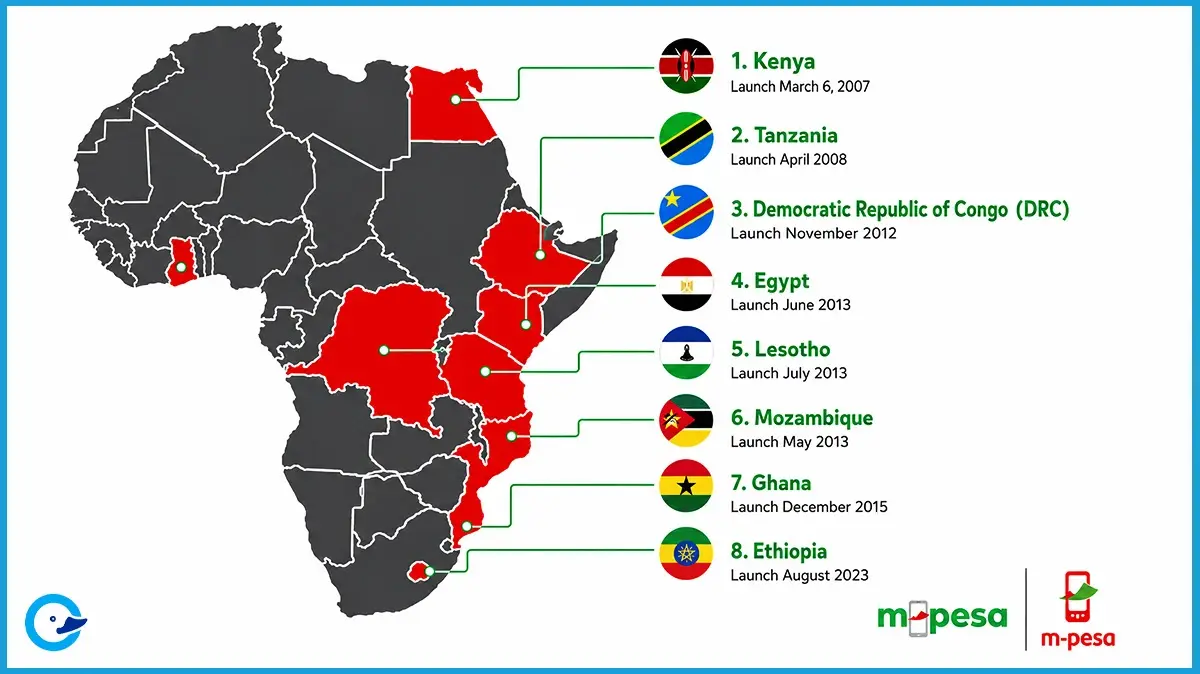

The service now covers eight countries in Africa: Kenya, Ghana, Democratic Republic of Congo (DRC), Egypt, Lesotho, Mozambique, Ethiopia and Tanzania, serving 60 million customers.

This article presents a list and relevant information on the countries where M-Pesa operates in 2026.

1. Kenya

Kenya is where M-Pesa was born. Safaricom launched it in March 2007 as a way to extend financial access to a population that largely lacked bank accounts.

The service took root fast, and today it is woven into the fabric of daily economic life — from settling utility bills and school fees to disbursing salaries and accessing micro-loans.

Over 90% of Kenyan adults now have access to mobile banking, a figure directly tied to M-Pesa's reach. The platform is Safaricom's primary revenue driver, accounting for roughly 40% of service revenue.

In Kenya alone, M-Pesa processes tens of billions of dollars in transactions each year, and its agent network spans every corner of the country, including rural areas that formal banks have never reached.

2. Tanzania

M-Pesa expanded to Tanzania in April 2008, launched by Vodacom. Early uptake was slower than anticipated, but the service found its footing after structural improvements and recommendations from the International Finance Corporation were implemented.

Tanzania's M-Pesa offering has since grown to include bill payments, airtime purchases, and microfinance loan repayments — moving well beyond simple person-to-person transfers.

3. Democratic Republic of Congo (DRC)

M-Pesa launched in the DRC in November 2012. The country presents a unique challenge: a vast territory with significant infrastructure gaps and a large unbanked population.

M-Pesa's agent-based model is well-suited to this environment, giving users cash-in and cash-out access without requiring a formal bank account.

The DRC has one of the continent's highest concentrations of active M-Pesa users relative to its banking penetration rates.

4. Mozambique

Mozambique came on board in May 2013. The service there covers the core M-Pesa use cases — money transfers, cash withdrawals, bill payments, and airtime top-ups.

Like other markets where formal banking infrastructure is limited, M-Pesa fills a critical gap by giving mobile phone users a reliable way to store and move money.

5. Lesotho

Lesotho joined the M-Pesa network in July 2013. It is among the smaller markets by population, but M-Pesa has become the dominant mobile financial service in the country.

For a nation where many residents work across the border in South Africa and send money home, a reliable mobile money platform addresses a practical need that traditional banking has historically failed to meet affordably.

6. Ghana

Vodafone launched mobile money services in Ghana in December 2015 under the brand "Vodafone Cash," utilizing the underlying M-Pesa platform technology.

Following Vodafone Group's complete exit from the Ghanaian market in early 2024, the network was acquired by the Telecel Group, and the service was officially rebranded to Telecel Cash.

The market has matured significantly since its inception, with the service functioning within a highly regulated mobile money ecosystem overseen by the Bank of Ghana.

While Ghana's mobile money sector is intensely competitive and heavily dominated by MTN Mobile Money, Telecel Cash remains an active player in the market, offering peer-to-peer transfers, bill payments, and merchant transactions.

Also read: How to Invest in US Stocks from Ghana

7. Egypt

Egypt launched M-Pesa in June 2013, making it the platform's first foray into North Africa. The service has remained operational in Egypt while other non-African expansion attempts, including Romania were eventually shut down.

Egypt gives M-Pesa access to one of Africa's largest populations and a market where mobile payment adoption has been growing steadily.

8. Ethiopia

Ethiopia is the newest market and arguably the most significant addition in terms of scale. Safaricom Ethiopia was granted a license to operate mobile money services in May 2023 and launched M-Pesa in August 2023.

By November 2025, M-Pesa Ethiopia had grown its active customer base to 3.4 million users over six months — a 174.8% increase year-on-year.

M-Pesa Ethiopia has since launched a telco-agnostic platform called M-Pesa LeHulum, which works with any SIM card, eliminating network barriers and allowing any mobile user to register and transact regardless of their carrier.

This is a first for the M-Pesa platform globally and positions the service for broader reach in a country where approximately 78% of the population lives in rural areas and only 35% of adults have access to formal bank accounts.

Ethiopia also broke ground on cross-border payments. In October 2024, M-Pesa extended its global service to Ethiopia, enabling mobile money transactions between Kenya and Ethiopia. With a population of over 120 million, Ethiopia represents the largest untapped market M-Pesa has ever entered.

M-Pesa Platform in 2026

M-Pesa Africa is a joint venture between Safaricom and Vodacom Group, established in 2020 after the two companies acquired the brand from Vodafone. That structure gives both operators direct control over product development, brand strategy, and expansion decisions across all eight markets.

The numbers as of 2026: 60 million customers, over 660,000 active agents, and more than $400 billion in annual transaction value.

Those figures reflect a service that has moved far beyond its origins as a simple transfer tool — M-Pesa now covers savings, credit, merchant payments, salary disbursement, international remittances, and bill settlement, operating through both USSD codes and smartphone apps.

For the 8 countries it serves, M-Pesa is not just a payment option. For millions of users, it is the only financial infrastructure they have access to.