It is possible to reach a point whereby you can live the rest of your life without ever working a single day. You wake up in your house near the beach or wherever your preference is, you bask in the sun, read a book, watch a movie, visit family or even go for vacations.

What you just lack is the personal finance formula for achieving financial independence, then once you have attained, you can chose to retire and live the life I have just described.

There are different formulas, however, there’s one that’s gaining lots of traction lately and it’s called FIRE (Financial Independence, Retire Early).

Whats interesting about this formula is that it gives you a number, many people just claim that they dream of getting rich, but question is, how rich, how much do you need to have so that you can say I am now rich.

FIRE gives you this figure,

Honestly, without this figure in mind, your path to being financially free will be vague.

You need to know how much and by the end of this article, you'll have the financial literacy needed to determine that number. Then after that, you’ll have the foundation for developing a strategy that will help you achieve financial independence early.

What is FIRE?

FIRE is an acronym for Financial Independence, Retire Early. It entails a lifestyle movement that was started to help people achieve early retirement. Followers of this movement achieve this FIRE number by choosing to live frugally, saving aggressively and disciplined and strategic investing.

The term was coined in the early 90s particularly in a book by Vicki Robin by the name Your Money or Your life. Since then, many people have adopted the concept in their own lifestyle.

Retire at 45 or earlier Not 65

For the longest time, we have always known that the year for retiring is 65. So if you started working at 20, it will take you 45 years to retire.

This means that you’ll have to work for nearly half of your life which is not good at all as losing your job implies losing your income.

It is even worse if working is not optional, meaning, if you don’t work then you’ll have no way of surviving.

In the modern age, people have grown to start embracing “living” and working half your life is not doing yourself justice at all.

What if there is a way to reduce the years and you get to retire early, let’s say 45 at most.

There is a formula for this and the best way is to start by calculating your FIRE number.

How to Calculate Your FIRE Number

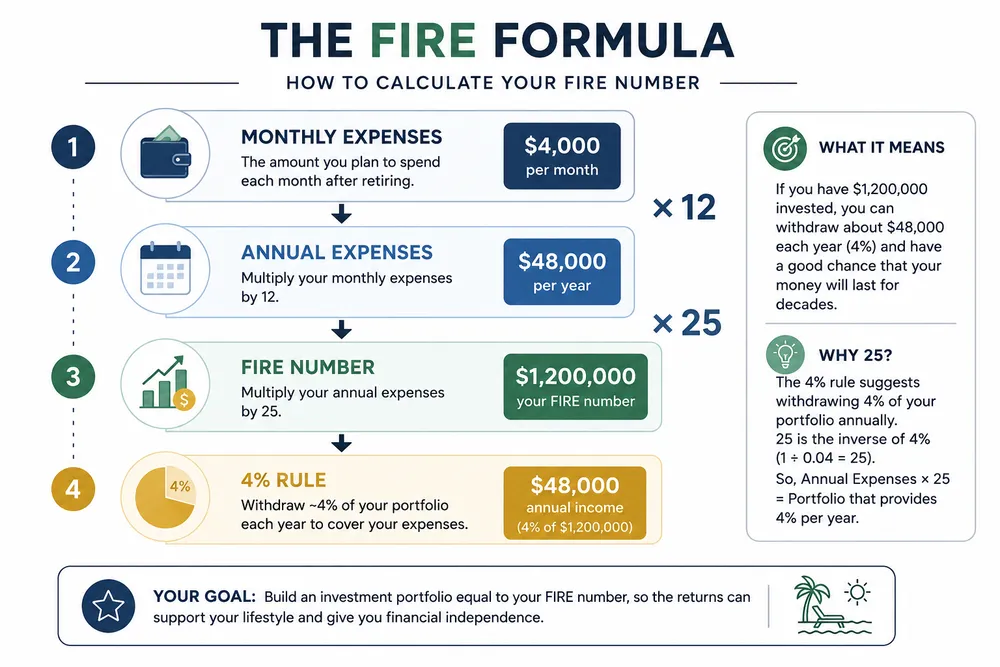

It is a very simple calculation once you know the formula. What you will need is an estimate of the amount of money you think you will need to spend every month after retiring.

For instance, one person can be comfortable spending $4,000/month while another person might want to spend $10k or even $50k, it all boils down to how you picture your lifestyle if you stopped working today.

For this calculation, we will use someone who is comfortable spending $4k a month. If you live in a low to middle-income country, let's say Kenya or Ghana, the figure might be lower, something like $1000 to $2000, approximately KES 129,290/ GHS 11,540 to KES 258,600/ GHS 23,080, factoring in the current exchange rate.

After you’ve decided how much you’d like to spend every month, multiply it by 12 so that you get how much you’ll spend in a year.

For our case assuming the person who we are calculating his FIRE number is called Richard.

If we multiply his monthly expenditure by 12, Richard’s annual expenditure will be $4000 X 12 = $48,000.

Now the formula for achieving financial independence and retiring early is:

FIRE Number = Annual Expenses × 25

You might be wondering, why multiply by 25? The answer lies in what's known as the 4% rule. The rule suggests that if you withdraw about 4% of your investment portfolio each year, your money has a good chance of lasting for decades. Multiplying your annual expenses by 25 means that 4% of your portfolio will roughly equal the amount you plan to spend each year.

For example, if Richard expects to spend $48,000 per year once he retires.

His fire number becomes,

$48,000 × 25 = $1,200,000.

Notice what happens. Four percent of $1.2 million is $48,000. In other words, Richard can withdraw the amount he needs each year without immediately depleting his investment portfolio.

Note: This formula applies regardless of the currency.

In this case, we have assumed Richard lives in the United States. So, if Richard was Ghanaian and he spent GHS 48,000 per year, still his fire number will be GHS 1.2 million. The same applies for a South African or living in UK.

Now, when you achieve this amount of money in your portfolio, then you can consider yourself financially independent. For Richard, he needs to have $1.2 million investment to be financially independent.

If you'd like to calculate your own FIRE number, use our FIRE Number Calculator.

For Richard, reaching a portfolio of $1.2 million means he can withdraw around $48,000 each year under the 4% rule. Since that matches his planned annual expenses, he has reached his FIRE number and can consider himself financially independent.

Your FIRE Number Is Only the Beginning

Now that you and Richard have established your FIRE number, the next question is, how many years will it take to get there?

Knowing your FIRE number is like knowing the destination of a journey. It tells you where you want to go, but it doesn't tell you how long the journey will take or the route you'll use to get there.

This is where many people stop. They calculate their FIRE number, get excited about it and never go any further.

The truth is, your FIRE number is only the first part of the personal finance formula. The second part is determining how long it will take you to achieve it.

How Long Will It Take to Reach Your FIRE Number?

To answer this question, you first need to know your current net worth.

Your net worth is simply the total value of everything you own minus everything you owe. It gives you a starting point.

Think of it this way. Richard now knows he needs an investment portfolio worth $1.2 million to become financially independent. But if Richard already has investments worth $300,000, he is much closer to his goal than someone starting from zero.

If you're not sure what your current net worth is, use our Net Worth Calculator.

Alternatively, read our guide on how to calculate your net worth to understand how the calculation works.

Once you've established your net worth, the next step is to decide how much money you're willing and comfortable investing every month. This is the amount that will move you from where you are today to your FIRE number.

Using Richard’s example, we already know his FIRE number is $1.2 million.

Now assume Richard has a current net worth of $300,000 and decides to invest $2,000 every month. Let's also assume his investments earn an average annual return of 10%.

Using these figures, Richard would reach his FIRE number in approximately 14 years to grow his portfolio from $300,000 to $1.2 million.

Now imagine Richard increases his monthly investment to $3,000 instead. His timeline immediately becomes shorter. If his investments earn a higher return, the number of years reduces even further. On the other hand, if he invests less or delays investing, it will take him longer to achieve financial independence.

This is why knowing your FIRE number alone isn't enough. You also need to know your starting point and how much you're investing every month. These three figures work together to determine when you'll become financially independent.

The Variables That Determine Your FIRE Timeline

There isn't a fixed number of years it takes to achieve FIRE because everyone's financial situation is different. However, there are a few variables that determine how fast or slow you'll get there.

The first is your current net worth. The more wealth you've already built, the shorter your journey.

The second is how much you're investing every month. Generally, the more you invest consistently, the faster you'll reach your FIRE number.

The third is the rate of return on your investments. A portfolio earning an average annual return of 10% will grow much faster than one earning 5%.

Lastly, there's time. The longer your investments remain untouched, the more compound interest works in your favour. This is why people who start investing early often achieve financial independence much sooner than those who delay.

These four variables work together to determine your FIRE timeline.

How to Reach Your FIRE Number Faster

If you've calculated your FIRE number and realised it will take longer than you'd like, don't worry. The good thing is that every variable in the formula can be improved.

You can increase the amount you invest every month by growing your income or reducing unnecessary expenses.

You can improve your investment returns by building a well-diversified portfolio and remaining invested for the long term instead of trying to time the market.

You can also start investing as early as possible. Time is one of the biggest advantages investors have because every additional year gives compound interest more time to grow your wealth.

The goal isn't simply to retire early. The goal is to build enough wealth so that working becomes a choice rather than a necessity.

Now you have the complete picture. You know your FIRE number, you know where you're starting from and you understand the variables that determine how long it will take to get there. The next step is to put the formula into practice and begin building your portfolio until your investments can comfortably fund the lifestyle you've chosen.