In Kenya today, credit is more available than ever. Getting a loan has become very easy, especially for young people today, compared to the past. Problem is, real financial literacy is still lagging behind.

TransUnion, one of Kenya’s major credit rating agencies, recently released a report showing that 1 in every 6 borrowers is already in default.

The warning signs are clear, and for anyone in their 20s or 30s, it’s a serious wake-up call.

Truth is, when credit/loans are used wisely, they have the potential of changing someone’s life, raising their financial status.

“Credit, when used wisely, can be a powerful enabler, opening doors to education, entrepreneurship, and personal growth,” said TransUnion CEO Morris Maina.

“But without a solid foundation in financial literacy, we risk seeing many young people excluded from future economic opportunities because of poor credit decisions made today.”

According to the study, first-time borrowers are particularly at risk. Many people in Kenya today, don’t fully understand how loan defaults, late payments, or even borrowing small amounts with high interest can be detrimental.

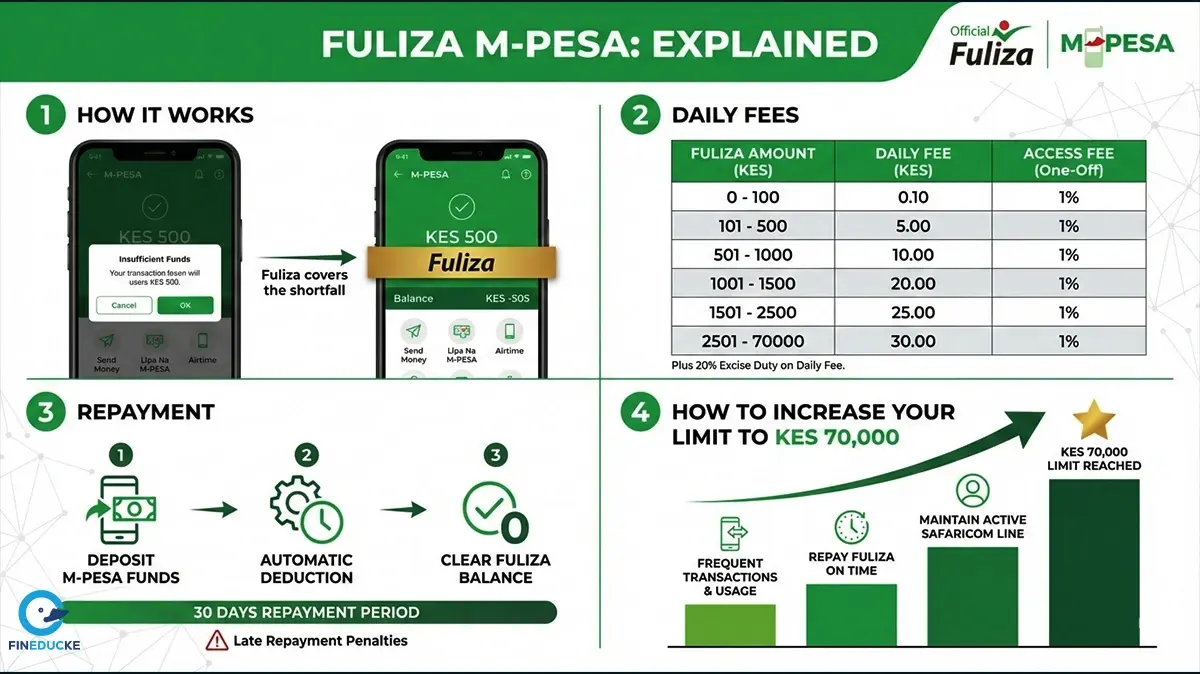

That Fuliza loan you take daily, if you calculate the interest over a year, you will be shocked.

We have normalized using credit e.g. Fuliza as if it’s our own money. And that’s where the problem is, we love easy money.

According to the FinAccess 2024 survey, formal financial access in Kenya has jumped to 84.8 percent. That’s a big milestone only that it doesn’t tell the full story.

Most people start their credit journey with digital loans, which are quick and easy to access. But what they don’t always see is the fine print: how compound interest adds up, how credit scoring works, or what happens when you miss payments.

This lack of understanding is proving costly. Worse among the Kenyan youth.

“Encouraging smart credit use isn’t just about personal finance; it’s about building a generation that can participate meaningfully in Kenya’s economy,” Maina added.

“When young people are given the tools to make responsible financial choices, the ripple effect is felt across families, communities, and the country at large.”

The financial pressure has shifted from personal to national. Kenya is now facing its worst rate of loan defaults in two decades. Recently, Fineducke analyzed the loans that President Ruto has borrowed compared to Uhuru and the late Kibaki, the findings? ALARMING!

Fresh data from the Central Bank of Kenya (CBK) shows that the percentage of non-performing loans, these are loans unpaid for over 90 days, findings show that they have risen to 17.6% as of June 2025, up from 17.4% in April.

“Increases in NPLs were noted in trade, personal and household, tourism and hotels, and building and construction,” said CBK Governor Kamau Thugge.

From a total loan book of Sh4.045 trillion, more than Sh712 billion is now at serious risk of not being recovered. That’s money banks expected back and truth is, they might not recover.

The CBK attributes this to job losses, stagnant incomes, and a rising cost of living. But those aren’t the only culprits.

Behind many of these defaults are choices made at a personal level, especially by young professionals trying to keep up appearances.

Personal finance coach and former banker, Kepha Obol, warns:

“Young people now habitually borrow to fund nights out, impulse purchases, or the latest gadget. What follows is a cycle of dependency, stress, and reduced financial health, a far cry from the soft life they sought.”

He’s right. The pressure to “look successful” is everywhere. From luxury dates to unplanned trips, this lifestyle creep can quietly drain your finances, worse if its financed using loans, common ones being digital loans.

It’s not just occasional borrowing, either. A past study found that at least 58% of young people aged 22–35 borrow mostly over weekends and at night, which suggests most of that money goes into leisure, not necessities.

The Digital Financial Services Association of Kenya (DFSAK) reports that Kenyans are now borrowing Sh500 million every day which is around Sh15 billion a month. All these money is borrowed through digital lenders. That’s a massive number for a population where financial literacy remains low.

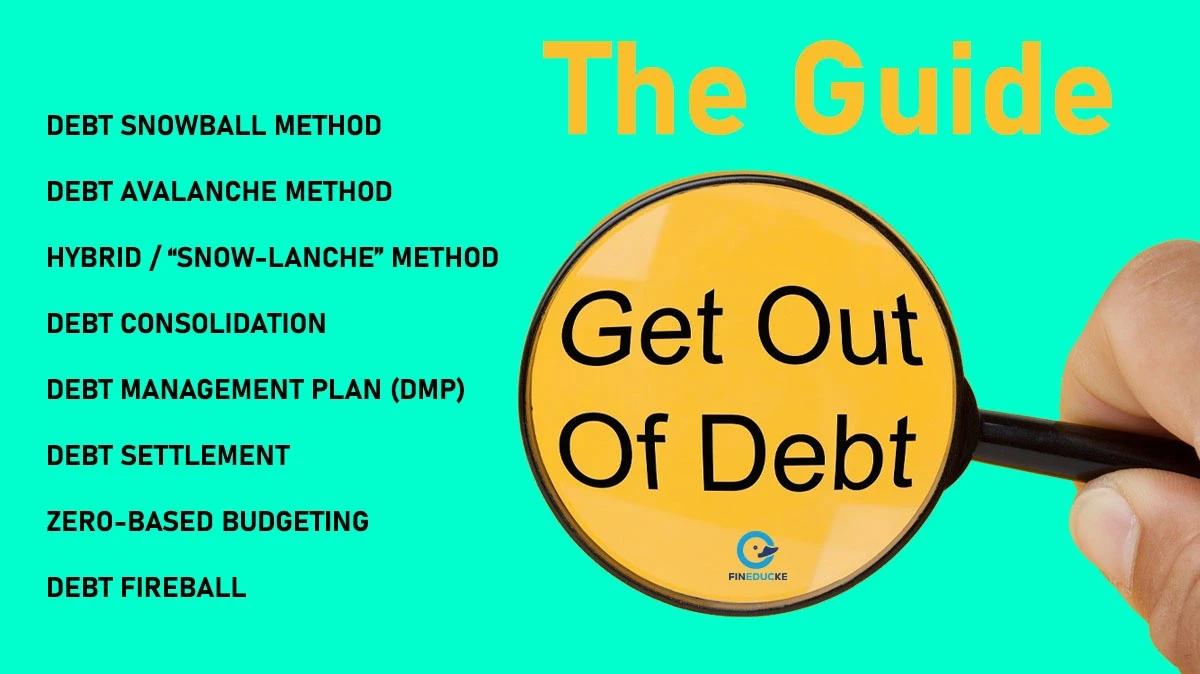

For those who are already in this cycle and trying to get out, there are practical ways to start reversing it. These proven strategies to pay off debt faster can help you regain control and move toward real financial freedom:

There is a dire need for people, especially Kenyan youth to embrace technology even in their finances. If budgeting and expense tracking is a challenge, then having a personal finance app can help ease the burden.

Tracking your expenses helps you understand your spending habits

When you categorize your expenses into food, rent, shopping, utilities, and fees you will easily learn your financial habits and gain insights into your spending and areas where you can save.

Credit isn’t the enemy. In fact, when managed well, it’s one of the most powerful tools for growth. But only if you know how it works.

It doesn’t matter if you’re applying for your first digital loan, chasing a dream business idea, or just trying to cover bills, the real question is, do you know what this loan will cost you tomorrow?

Because understanding money is more than budgeting, it's about building the life you actually want without sacrificing your future to fund today’s fun and this is not to dismiss YOLO.

If you are a Kenyan youth and you want to avoid the debt trap? Start by:

And most importantly, learn before you borrow.

I’m Clinton Wamalwa Wanjala, a financial writer and certified financial consultant passionate about empowering the youth with practical financial knowledge. As the founder of Fineducke.com, I provide accessible guidance on personal finance, entrepreneurship, and investment opportunities.

i understand