People ask me all the time if they should use their home equity to clear out bad debt. My answer is almost always yes. But only if you do it right. Do it wrong and you just stretch a three year problem into a thirty year nightmare.

Let me be completely straight with you. I see folks every week drowning in personal loans, car finance, and Afterpay. Meanwhile their house value has jumped up by two hundred grand since they bought it. That equity is sitting there doing absolutely nothing. We can put it to work.

I had a couple in my office last Tuesday. Let us call them Dave and Sarah. Great jobs. Nice house in Brisbane. But they were bleeding cash. They had a fifty thousand dollar car loan at 9 percent and about thirty thousand on credit cards ticking over at a gross 21 percent. They were paying over two thousand dollars a month just to keep the wolves from the door. Not paying down the principal. Just surviving.

We pulled out the calculator. By rolling that eighty thousand dollars of bad debt into their home loan at 6.2 percent, their total monthly repayments dropped by twelve hundred dollars. That is $14,400 a year back in their pockets. That is real money.

But here is the catch. You need discipline.

I refuse to help clients consolidate debt if they plan to keep the credit cards open. Period. You consolidate, you cut the plastic. Otherwise you end up with a bigger mortgage and a brand new pile of credit card debt in twelve months. I've seen it happen. It's ugly.

The banks will look at your Loan to Value Ratio. We call it LVR. Ideally you want to keep your total borrowing under 80 percent of what the property is worth. Go over that and you get slapped with Lenders Mortgage Insurance. Nobody wants to pay LMI if they can avoid it. It's just dead money going straight to the bank's insurer.

You need a fresh valuation on your property to see what you actually have to work with. If you happen to be up north, getting a good mortgage broker Queensland based is a smart move. Local brokers know the exact valuers the banks use and understand exactly how regional property markets are moving. They can tell you straight up if your equity expectations are realistic or completely cooked.

Don't just add the old debt to your main loan and forget about it. That is a massive rookie mistake.

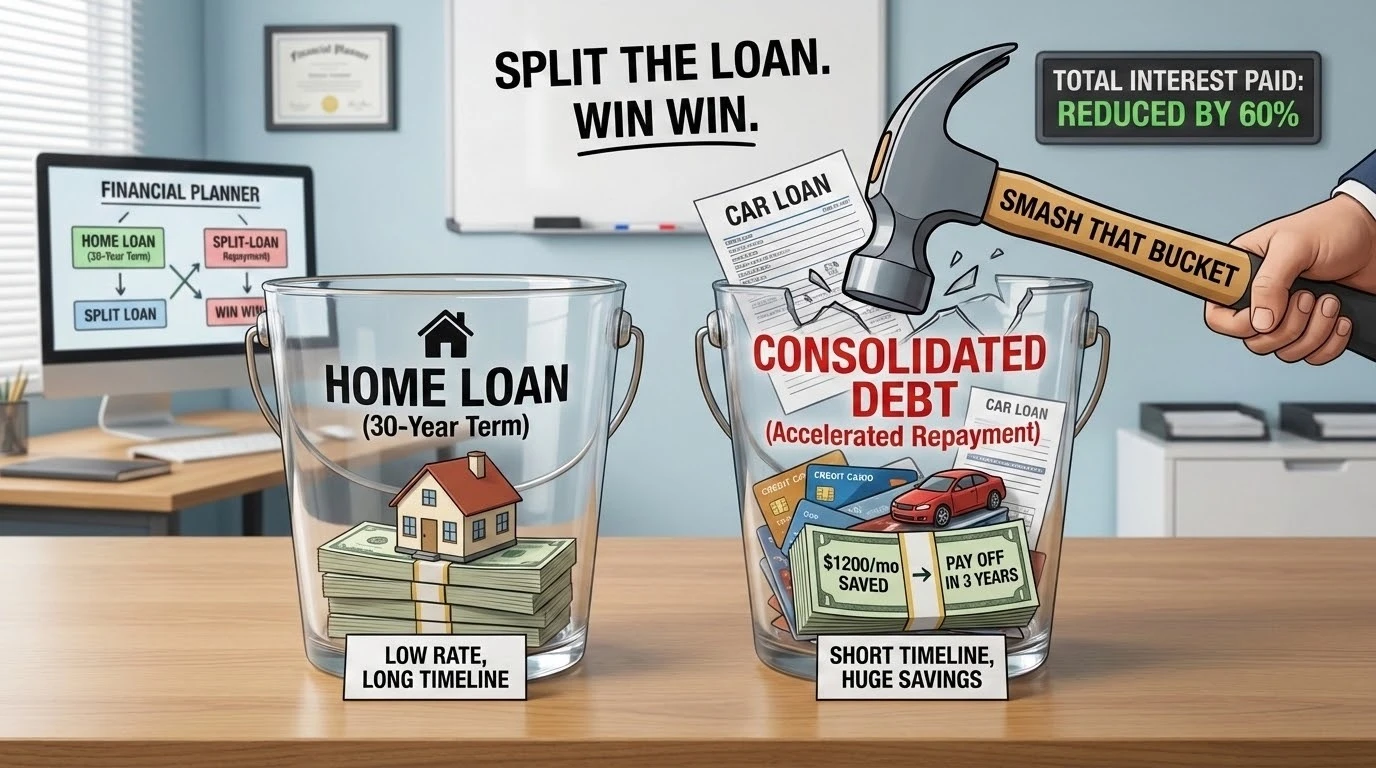

Say you roll a thirty thousand dollar car loan into a thirty year mortgage. Sure, the interest rate is way lower. But you are paying that lower rate for three decades. You end up paying more interest over the long haul. A car doesn't last thirty years.

The fix is simple. We split the loan. We put your home loan in one bucket. We put the consolidated debt in another bucket. Then we smash that second bucket. We set the repayments on that specific portion artificially high. You use that twelve hundred dollars a month you saved to pay off the car and the cards in three years instead of thirty. You get the low interest rate, but you keep the short timeline. Win win.

Refinancing isn't just clicking a button on an app. It involves discharging your current mortgage and registering a new one. It involves actual paperwork. The banks are notoriously slow. They will drag their feet because they don't want to lose you.

This is where people get lazy and try to do it all themselves. Bad idea. You want professionals handling the transfer. Finding a sharp Refinancing mortgage lawyer makes the process completely painless. They handle the settlement. They deal with the outgoing bank. They make sure the title transfers cleanly without you spending three hours on hold listening to terrible elevator music. Don't skimp on good advice.

Look at your statements tonight. Calculate exactly what you pay in interest every single month on personal debt. Then look at your property value. If you have the equity and the discipline to change your spending habits, rolling that debt into your mortgage is a total no brainer.

Stop paying the banks extra money for absolutely no reason. Take control of your equity. Pay off your debts on your own terms.

The Fineducke Team is a group of passionate writers, researchers, & finance enthusiasts dedicated to helping the youth make smarter money decisions. From saving tips, investment ideas to digital income guides, our team works together to bring you easy-to-understand, practical content tailored for everyday life believing financial education should be simple & relatable.

Leave a Comment:

Please log in to leave a comment.

Comments:

No comments yet. Be the first to comment!