Money can be tricky. One month you feel like you’re on top of your finances, and the next you’re wondering where your salary disappeared to. Whether you’re hustling in Nairobi, farming in Eldoret, or running a small business in Mombasa, we can all agree on one thing; good financial planning can save you from unnecessary stress and open doors to a more secure and fulfilling future.

So, how do you get your finances in order without feeling restricted? Here are practical personal finance tips designed for my beloved Kenyan brothers and sisters to help you take control of your money and build lasting financial security.

Before you can plan your finances effectively, you need to understand your true income. Many people make the mistake of budgeting based on their gross salary (this is the amount they see on your offer letter) without considering the mandatory deductions that reduce their take-home pay. In Kenya, deductions like PAYE (Pay As You Earn tax), SHIF (Social Health Insurance Fund), and NSSF (National Social Security Fund) can significantly reduce what you actually receive. Some employers may also deduct for loans, SACCO contributions, or other benefits.

Your real income is what hits your bank account or MPESA after all these deductions. When budgeting or making other financial decisions, this is the amount that you are supposed to work with. If you ignore this, you will often find yourself overspending, having unpaid bills, or relying on expensive mobile loans to survive the month.

If you have side hustles, freelance gigs, or small businesses, treat that income as a bonus rather than your primary spending money. Ideally, direct side hustle income into savings, investments, or debt repayment instead of lifestyle upgrades. This mindset helps you grow financially without feeling stuck in a cycle of living paycheck to paycheck.

Taking the time to understand your net income, down to the shilling, gives you clarity, reduces financial stress, and lays the foundation for smarter money management.

A budget is not about restricting yourself, it’s about telling

A budget is a tool that you use to tell your money where it should go, its not a tool that you use to restrict yourself. If you don't create a budget, then you will often keep wondering where your money went. Also, without a budget or a good one for that matter, it’s easy to overspend on non-essentials and struggle with bills before the month ends. One of the easiest frameworks that you can use is the 50/30/20 rule:

This approach works because it creates balance—you cover your needs, enjoy life a little, and still secure your future.

Did you know that in Kenya, over 60% of salaried workers run out of money before their next paycheck, forcing them to borrow from mobile loans? Budgeting can break that cycle. If spreadsheets feel overwhelming, try simple tools like YNAB, Mint, or even MPESA mini-statements to see where your money really goes.

The goal is awareness and control. Once you know your spending habits, you can adjust and prioritize what truly matters, making your money work for you instead of the other way around.

Most people save whatever remains after they’ve spent, and let’s be honest—there’s usually nothing left. The smarter approach is to pay yourself first. The moment your salary or income comes in, set aside a specific portion for savings before you touch anything else. Think of it as paying a non-negotiable bill to your future self.

Start small if you must. Even 500 shillings a week adds up to about 26,000 shillings a year, which can cover emergencies like a medical bill, car repair, or school expense. Over time, aim to build an emergency fund that covers at least 3–6 months of living expenses. This cushion protects you from relying on expensive loans during tough times.

For short-term savings, use Saccos, money market funds, or fixed deposit accounts. Saccos are popular in Kenya because they encourage discipline and often pay higher dividends than banks. Money market funds are also great because they offer better returns than a regular savings account while keeping your cash accessible.

When you save first, you prioritize financial security, reduce stress, and create room for long-term goals like buying a home, starting a business, or retiring comfortably.

It is very important to be cautious and have a plan before borrowing. In Kenya, getting credit has become easier than ever—from mobile apps to credit cards—but this convenience also comes with temptation. One small loan can quickly turn into a lifestyle you can’t sustain.

If you must borrow, do it for the right reasons—things that either grow your income or improve your long-term stability. That could be investing in a business, paying for a skill, or purchasing an asset that appreciates in value. Never borrow for fleeting pleasures or status symbols.

Credit cards can be powerful tools when used wisely. They help you build a solid credit history, which can make it easier to qualify for a mortgage or business loan later. But the trap comes when you carry a balance month after month. Interest rates can go up to 30% per year, turning a small expense into an expensive mistake.

A simple rule: if you can’t pay it off in full when the bill arrives, don’t swipe it. For daily spending like groceries or airtime, stick to a debit card or MPESA—you can’t overspend what you don’t have.

Responsible borrowing is about intent and discipline. Every loan should have a purpose and a repayment plan before you even apply. Borrow with a clear reason, not out of impulse.

Debt itself isn’t the enemy, it can actually help your financial growth if managed wisely. A well-planned loan can open doors to opportunities like furthering your education, starting a business, or investing in property. But when misused, debt becomes a trap that quietly eats away at your income through endless interest payments.

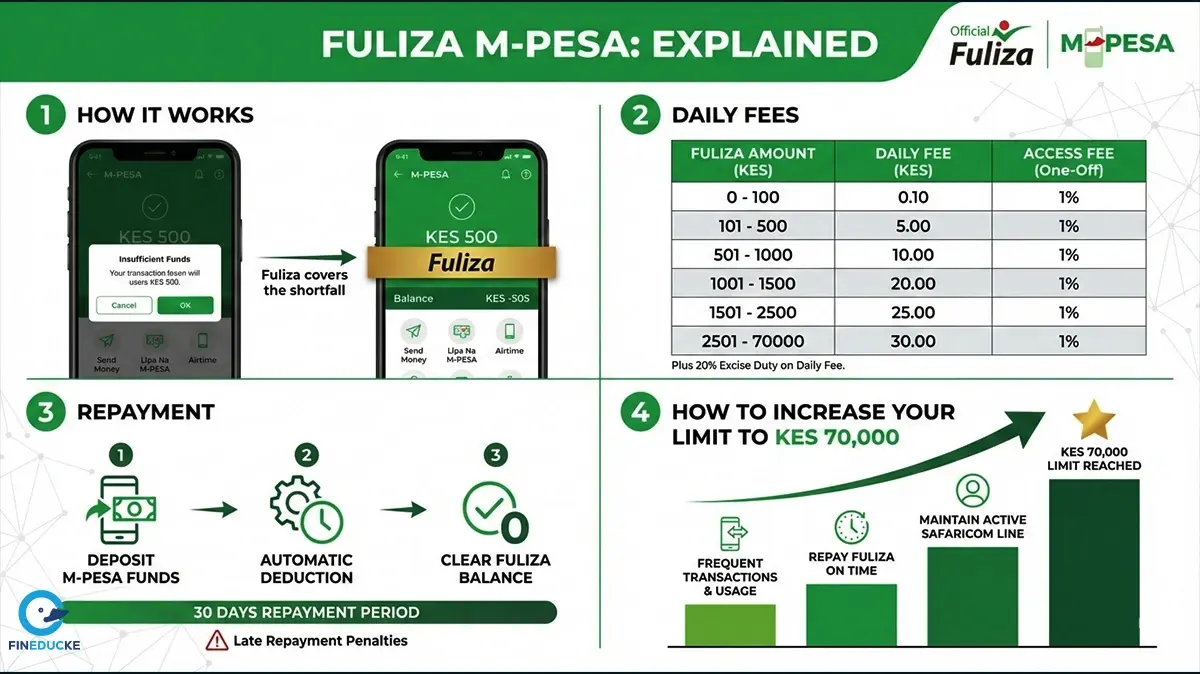

In Kenya, many people fall into the mobile loan cycle—borrowing from M-Shwari, Hustler Fund, Tala, or Branch to cover lifestyle expenses like eating out or buying non-essentials. These short-term loans may seem harmless at first, but their high interest rates can quickly spiral out of control.

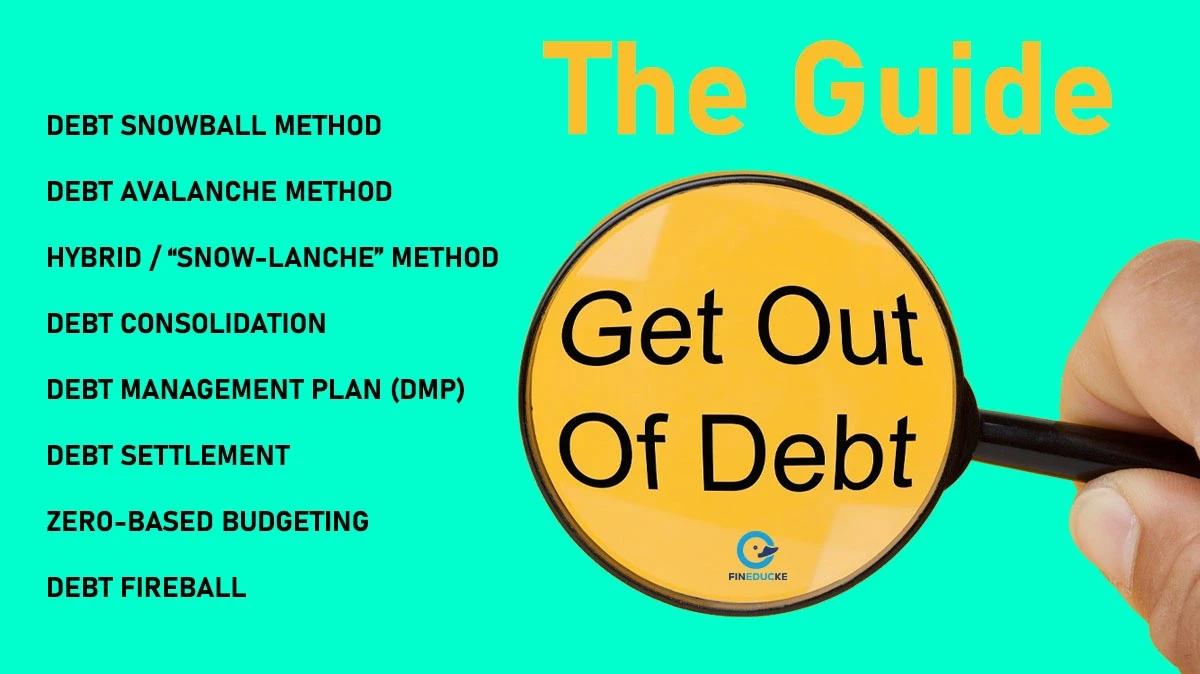

If you already have debt, focus on taking control instead of panicking. Start by listing all your loans and noting their interest rates. Then, tackle the most expensive ones first—this is called the debt avalanche method and helps you save money over time. Alternatively, if you need a psychological boost, begin with the smallest debts first using the debt snowball method to build momentum.

Avoid borrowing to pay off another loan unless you’re consolidating at a lower rate. Otherwise, you’ll only sink deeper. And if possible, join a Sacco, where interest rates are often fairer and repayment terms more flexible.

To learn about different methods that you can use to repay debt, Check out this guide on Top 8 Debt Repayment Methods. It will help you understand the best strategy you can use to pay different types of debt.

Remember, if used well, debt can help you move forward and when its mismanaged, it will hold you back big time. The goal here isn’t to avoid debt entirely but to make it work for you and not against you.

Your credit score is like your financial reputation. In Kenya, it’s tracked by the Credit Reference Bureau (CRB) and determines how lenders view you. Many people only realize how important their CRB status is when they’re denied a bank loan, Sacco credit, or even a hire purchase plan.

A bad credit record can come from something as simple as delaying a small mobile loan repayment, missing a utility bill, or defaulting on a Hustler Fund loan. The good news is that you can avoid this by practicing good financial habits. Always pay your loans and bills on time, even if it’s just a small amount.

It’s also important to regularly check your credit report for errors or outdated information that could hurt your score. You can request a free credit report once a year from agencies like Metropol, TransUnion, or CreditInfo.

Maintaining a healthy credit score opens doors to better financing options, lower interest rates, and faster loan approvals. Think of it as building trust with lenders—responsible borrowing today makes it easier to access bigger opportunities tomorrow.

Personal finance isn’t just about surviving today—it’s about creating stability and security for the years ahead. Many Kenyans focus on short-term needs and forget about retirement, family protection, and building a lasting legacy. But planning ahead gives you peace of mind and ensures your loved ones are taken care of even in your absence.

Start with retirement savings. If you’re employed, maximize your contributions to a pension scheme. If you’re self-employed, consider setting up a personal retirement savings plan or contributing to an individual plan like those offered by insurance companies. The earlier you start, the more you benefit from compound interest, meaning your money grows faster over time.

Next, think about your family. Writing a will is essential, no matter your age. It ensures your property and assets are distributed according to your wishes, avoiding family disputes.

Finally, look into affordable investment options like government bonds, Treasury bills, or unit trusts. They are relatively low-risk and accessible even with small amounts, allowing you to build wealth steadily.

Planning for the future isn’t about fear—it’s about making sure your hard work today translates into lasting financial security for you and your family.

One unexpected hospital visit can wipe out years of savings, and in some cases, even push families into debt. That’s why insurance is not a luxury—it’s a financial safety net. At the very least, every Kenyan should have NHIF (National Hospital Insurance Fund) to cover basic medical needs. The monthly contribution is affordable, starting from as low as KES 500 for informal workers, yet it can significantly reduce out-of-pocket hospital costs.

If you have dependents, it’s wise to go beyond NHIF. Consider private medical insurance for more comprehensive coverage. Also, think long term: life insurance ensures your family can maintain their lifestyle even if you’re no longer around, while education policies can guarantee your children’s school fees are secure no matter what happens.

Insurance can also protect your property and business. For example, a simple home cover or business cover shields you from unexpected losses like fires, theft, or natural disasters.

Many people avoid insurance because they see it as an unnecessary expense. In reality, it’s a small cost compared to the financial devastation of being unprepared. With the right cover, you protect not just your money, but also your family’s future.

Taxes are unavoidable, but many Kenyans end up paying more than they should simply because they don’t understand available tax reliefs and deductions. This is literally free money on the table, yet it goes unused.

For instance, contributing to a registered pension plan not only helps you save for retirement but also reduces your taxable income. The Kenya Revenue Authority (KRA) allows tax relief on contributions of up to KES 20,000 per month or 240,000 per year, meaning you pay less PAYE tax. Similarly, if you have a mortgage on a primary residence, you can claim mortgage interest relief, reducing your tax burden further.

If you pay for life insurance policies, you’re also entitled to an insurance tax relief of 15% of premiums paid, up to a maximum of KES 60,000 per year.

The key is keeping organized financial records—receipts, statements, and certificates. And if you’re unsure, consult a licensed tax agent or accountant to help you optimize your taxes.

By understanding and using tax reliefs wisely, you keep more of your hard-earned money working for you instead of giving it all away unnecessarily.

Being financially disciplined doesn’t mean you should deny yourself all pleasures. Money is also meant to be enjoyed, but in a balanced way. Once you’ve handled your essentials, saved, and invested, it’s okay to set aside a small portion for personal treats. Maybe it’s a weekend trip to the Coast, upgrading your phone, or enjoying a nice dinner with friends. The key is planning for these rewards in your budget, so they don’t disrupt your financial goals. When you reward yourself occasionally, you stay motivated and avoid feeling deprived, making it easier to stick to your long-term money plan.

Personal finance is a journey, not a one-time fix. Start small, stay consistent, and don’t be afraid to ask for help from a financial advisor or trusted mentor. Even with Kenya’s rising cost of living, simple habits like budgeting, saving, and investing wisely can give you the peace of mind you deserve.

I’m Clinton Wamalwa Wanjala, a financial writer and certified financial consultant passionate about empowering the youth with practical financial knowledge. As the founder of Fineducke.com, I provide accessible guidance on personal finance, entrepreneurship, and investment opportunities.

Leave a Comment:

Please log in to leave a comment.

Comments:

No comments yet. Be the first to comment!